Published April 21, 2018

This is the second in a series of essays on my learnings and findings from a six month marketplace research project. There has been a lot written about online marketplaces and our goal was to test these theories by exploring patterns from a broader set of companies. We started by making a list of every marketplace founded, creating a list of 4,500 companies from Crunchbase, Pitchbook, and other sources. We collected public data to classify and compare these companies and identify patterns in marketplaces that became successful (read more about the approach).

Sharing economy marketplaces have become the preferred form of marketplaces for entrepreneurs, but they have worse unit economics than traditional marketplaces and require almost 3 times as much funding to achieve the same revenue.

Sharing economy marketplaces have individuals on the supply side of the marketplace, while traditional marketplaces have companies on the supply side. For example, Airbnb has mostly individual hosts while Hotels.com has companies (hotels) as suppliers.

Sharing economy marketplaces have become common despite lower capital efficiency and less attractive unit economics

Since 2007, individual-driven marketplaces like Uber have almost doubled in popularity. Of the 459 marketplaces we analyzed, 56% had individuals as suppliers (e.g. Airbnb), 33% of them had companies as suppliers (e.g. Hotels.com), and 12% had both companies and individuals (e.g. Amazon).

By focusing on individuals, these sharing economy marketplaces typically recruit far more suppliers than traditional marketplaces. By the end of least year, Airbnb had attracted 4 million hosts to Booking.com’s 1.5 million even though Booking.com was founded 12 years earlier and has revenues more than double that of Airbnb.

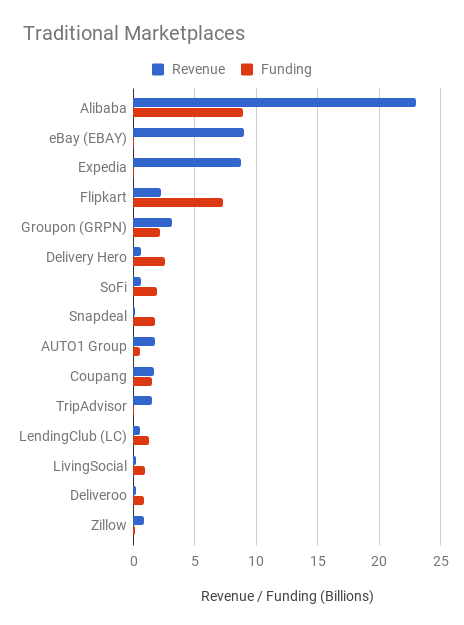

Sharing economy marketplaces tend to be far less capital efficient than traditional marketplaces, raising 50% more financing to achieve almost half the revenue:

| Sharing Economy Marketplaces | Traditional Marketplaces | |

| Avg Revenue / Funding | 5.71 | 14.37 |

| Average Funding | $207,424,863 | $253,255,675 |

| Average Revenue | $135,782,620 | $458,199,496 |

Lower capital efficiency is driven primarily by lower average revenue per supplier and higher churn compared to traditional marketplaces.

For an example of this, see Booking.com, which has rapidly scaled its number of bookable properties from 500k in 2014 to over 1.7 million in 2018. This growth has been largely from the “alternative accommodation market” that is more similar to Airbnb’s core supply base. Then-CFO of Priceline Dan Finnegan points out the financial differences with these individual-driven suppliers:

The new alternative accommodation business is somewhat less profitable from a partner services perspective. So there are less rooms for property, a lot of properties still to go and gather, and then, typically, requiring a little bit more help in working with our service because they’re less sophisticated than the hotel properties that we had initially worked with. – Q3 2017 PCLN Earnings Call

In “alternative accommodations” there are fewer rentable rooms for each property but there are still costs to acquire and onboard each property. For every rentable room, the acquisition cost is higher and the service cost is higher.

Individual supplier platforms also experience high rates of a unique type of involuntary churn from suppliers that traditional marketplaces don’t experience. Uber drivers get sick of driving and Airbnb hosts get tired of sharing a bathroom with strangers. 52% of suppliers on labor platforms like Uber quit driving within a year and 56% of suppliers on capital platforms like AirBnB stop hosting guests on any platform within the first 12 months. These attrition rates do not include suppliers leaving for competitors (e.g. leaving Uber to go to Lyft), they are specifically the number of suppliers that decide to leave the industry completely.

Company supplier platforms experience much lower rates of involuntary churn from their suppliers. Restaurants are commonly cited as one of the riskiest businesses to start, but the failure rate of restaurants (17% of restaurants fail in the first year) is far lower than the quitting rate of sharing economy marketplaces.

These rates shouldn’t be surprising when you consider that 55% of Uber drivers use Uber to earn supplemental income, working less than 15 hours per week. Sharing economy marketplaces like Airbnb and Uber also benefit from the part-time nature of their suppliers, since the supplier pool grows when demand grows:

The need for rides (and therefore drivers) at music festivals or seasonal events or in a vacation town like Tahoe are bursty. That said, these same holiday weekends are when people searching for supplemental income are free from the primary occupation and can make the voluntary decision to earn more money. – Bill Gurley

Airbnb and Uber are incredible businesses, and the conclusion of this post is not that company-driven marketplaces like Groupon and OpenTable are better than sharing economy marketplaces, but that they need to manage suppliers much differently.

Marketplace with companies as suppliers, particularly those with a Single-Player mode, can spend more to acquire suppliers and invest more in making them successful. By comparison, sharing economy marketplaces need to focus on developing product mechanics and incentives that constantly attract new suppliers to the platform.

eBay has transitioned from being a sharing economy marketplace to a hybrid that includes professional sellers, retail chains, and individual consumers. This is a common pattern and Josh Breinlinger makes the point that the number of full timers on a marketplaces is a key driver of marketplace health. eBay’s Powerseller program, Etsy’s 10k club, and Airbnb’s Plus host program encourage individual suppliers to become professionals that act more like companies in that they rely on the platform more and churn less. With professional suppliers, these marketplaces can invest more in tools and services to make those suppliers be successful.

Do you have a theory for why sharing economy marketplaces have raised so much more money than traditional marketplaces? Leave a comment here or send me an email (marketplaces at elichait.com)

Thanks to Elaine Hsu, Corey Reese, Miles Skorpen, Wendy Lin, and Nima Wedlake for reading drafts of this post and providing feedback.

Footnotes

- Only includes marketplaces where we had revenue and funding data. Excludes Amazon in charts for scale reasons only.